Introduction: Why These Terms Are Constantly Confused

Ask ten managers to explain the difference between compliance, risk, and audit, and you’ll usually get ten slightly different answers — all confident, all incomplete.

That’s not because people are careless.

It’s because, inside most organisations, these functions intersect around the same failures: controls breaking, regulators asking questions, incidents escalating.

But here’s the issue most businesses don’t notice until it hurts:

When roles blur, accountability disappears.

- Compliance starts acting like risk

- Risk gets treated like audit

- Audit gets blamed for problems it doesn’t own

In fintech especially — where regulation is dense, growth is fast, and margins are thin — this confusion creates governance blind spots that only show up after damage is done.

This article clears that up.

No theory for theory’s sake.

Just one goal: who owns what — and who doesn’t.

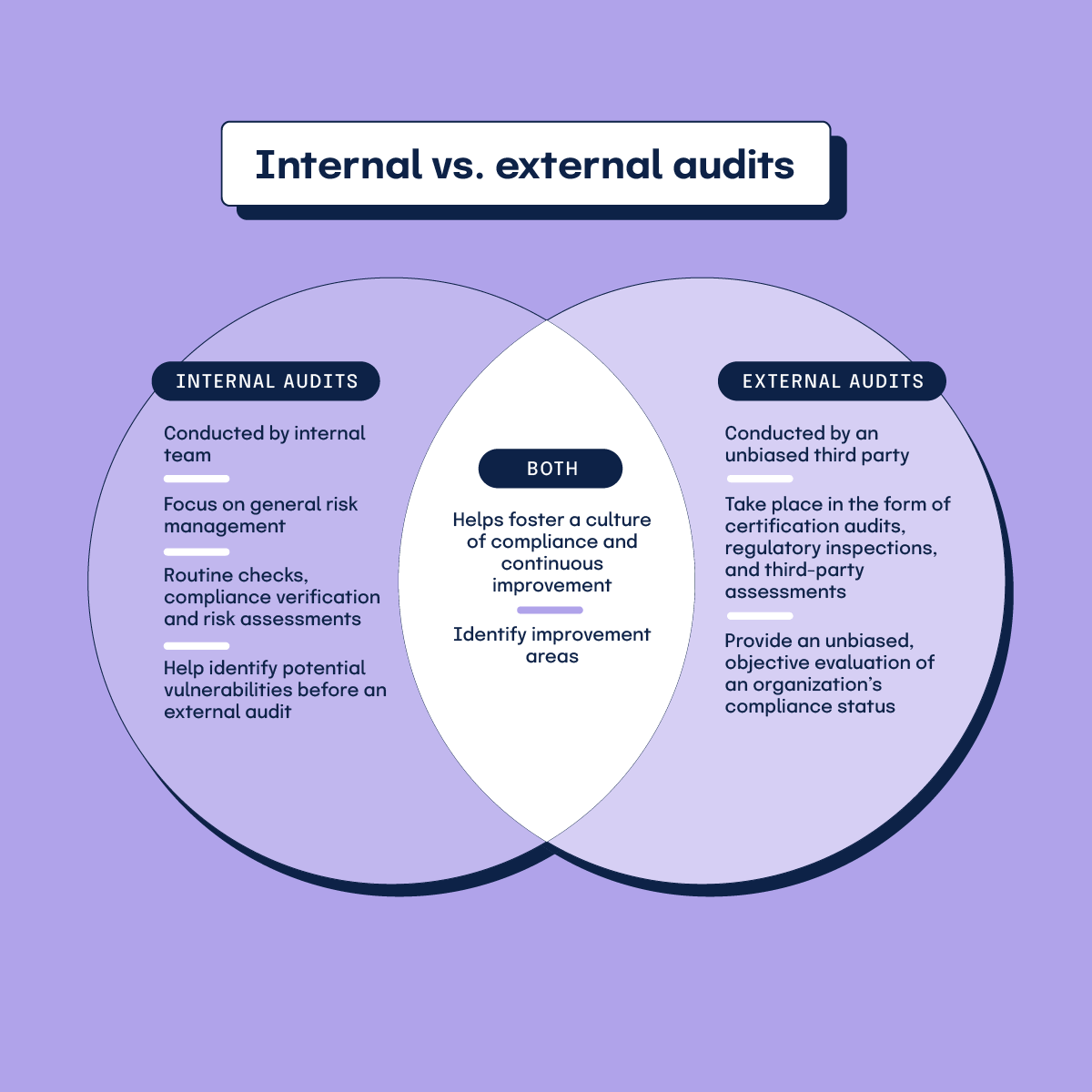

Compliance vs Risk vs Audit — What Each Function Actually Does

Before diving into detail, anchor the distinction properly:

- Compliance asks: Are we following the rules?

- Risk management asks: What could stop us achieving our objectives?

- Audit asks: Are the first two actually working as claimed?

Same environment.

Different responsibilities.

No overlap in ownership.

Why Compliance, Risk, and Audit Get Mixed Up in Real Organisations

The confusion isn’t academic. It’s structural.

1. All Three Interact With Controls

Policies, approvals, monitoring, reporting — every function touches controls. That creates surface similarity, not shared accountability.

2. SMEs Collapse Roles Out of Necessity

In fintech SMEs, it’s common to see:

- “Risk & Compliance” combined

- Control owners reviewing their own work

- Audit outsourced and misunderstood

This isn’t governance by design. It’s governance under constraint.

3. Failures Trigger All Three at Once

When something goes wrong:

- Compliance handles remediation

- Risk reassesses exposure

- Audit reviews what failed

Because they appear together after incidents, people assume they do the same job.

They don’t.

What Compliance Actually Owns

The Core Purpose of Compliance

Compliance exists to ensure adherence to external obligations and internal rules derived from them.

Its job is conformance — not optimisation, not strategy.

What Compliance Owns in Practice

In a fintech SME, compliance typically owns:

- Interpretation of laws and regulations

- Creation and maintenance of policies

- Compliance monitoring and testing

- Regulatory reporting

- Staff training on obligations

Example:

A payments fintech must comply with AML, sanctions, data protection, and consumer protection rules. Compliance defines what must be followed and how adherence is demonstrated.

What Compliance Does Not Own

This is where most organisations go wrong.

Compliance does not own:

- Business risk decisions

- Risk appetite

- Whether controls are commercially “enough”

- Independent assurance

Compliance says: “This is required.”

It does not say: “This is sufficient.”

What Risk Management Does Differently

The Core Purpose of Risk Management

Risk management exists to protect objectives, not rules.

It looks forward, not backward.

Risk asks:

- What could go wrong?

- How likely is it?

- How severe would the impact be?

- What are we doing about it?

And critically:

Some risks are consciously accepted.

Compliance doesn’t accept risk.

Risk management evaluates and decides.

What Risk Management Owns

In fintech SMEs, risk typically owns:

- Enterprise risk identification

- Risk assessment and prioritisation

- Risk appetite and tolerance

- Control design from a risk perspective

- Ongoing risk monitoring

Example:

A fintech may fully comply with regulation when launching a new lending product — yet still take on:

- Credit concentration risk

- Model risk

- Liquidity risk

Compliance can approve.

Risk may still escalate.

That’s not disagreement.

That’s correct governance.

Where Audit Fits — And Where It Doesn’t

The Core Purpose of Audit

Audit provides independent assurance. Nothing more, nothing less.

Audit does not:

- Design controls

- Manage risks

- Fix issues

- Prevent failures in real time

Audit answers one question:

Are governance, risk, and compliance processes designed and operating as management claims?

What Audit Owns

Audit owns:

- Independent evaluation

- Objective testing

- Assurance to senior management or the board

- Reporting weaknesses without fixing them

Independence is not optional.

Once audit starts “helping,” assurance is compromised.

What Audit Does Not Do

Audit does not:

- Own compliance

- Accept risk

- Approve controls

- Act as management

If audit is blamed for failures, the organisation has already misunderstood its role.

Practical Fintech SME Examples

Example 1: AML Monitoring Failure

- Compliance: AML policy exists, training completed

- Risk: Transaction monitoring thresholds never updated as volumes scale

- Audit: Later identifies ineffective monitoring

Responsibility breakdown:

- Compliance met obligations

- Risk failed to reassess exposure

- Audit identified the issue — after the fact

Audit didn’t fail.

Risk ownership did.

Example 2: Rapid Product Expansion

- Compliance: Product meets regulatory requirements

- Risk: Operational capacity risks ignored

- Audit: Flags control gaps post-launch

Compliance was correct.

Risk assessment was incomplete.

Audit arrived late — by design.

That’s how the system works when roles are clear.

The One Rule That Prevents Most Confusion

If you remember nothing else, remember this:

Compliance defines obligations.

Risk evaluates exposure.

Audit verifies reality.

When one function starts doing another’s job:

- Accountability blurs

- Assurance weakens

- Management gets false comfort

In fintech, where speed hides risk, clarity isn’t optional — it’s protective.

Conclusion: Role Clarity Is a Control in Itself

Organisations don’t fail because they lack frameworks.

They fail because nobody knows who owns what.

Clear separation between compliance, risk, and audit:

- Surfaces issues earlier

- Improves decision quality

- Strengthens regulatory trust

- Stops responsibility ping-pong

Most importantly, problems get owned, not passed around.

In practice, role clarity is one of the strongest controls you can have.